Fixing GST errors

If your business made an error when reporting GST claims on a past business activity statement (BAS), you may be able to correct it on the next BAS.

Errors are mistakes made when completing a BAS that would result in your business paying too much tax (credit error) or paying too little tax (debit error).

Credit errors

Credit errors can include:

- reporting a GST sale twice;

- overstating the GST on sales;

- omitting or understating a decreasing GST adjustment or overstating an increasing GST adjustment.

You can correct a credit error on a later BAS that is lodged within the period of review for the earlier reporting period.

The period of review starts on the day you lodge your BAS and ends four years and one day later.

If a credit error relates to GST credits, there is an additional time limit. You cannot correct an error to claim additional GST credits where the four-year credit time limit for claiming those GST credits has expired.

Debit errors

Debit errors can include:

- failing to include GST on a taxable sale;

- understating the GST on sales (e.g. reporting a lesser amount for GST on sales, rather than the correct amount);

- overstating GST credits (e.g. claiming GST credits for a purchase twice).

Time limits apply for the correction of a debit error from the time the debit error occurred (not

when it was discovered).

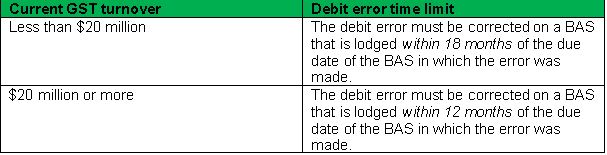

You can correct a debit error on a later BAS only if it is lodged within the debit error time limit that corresponds with your current GST turnover as shown in the table below.

If the debit error time limit has expired, you need to revise the period that contains the error if the period of review has not yet expired.

There is a debit error value limit. This means that you can correct a debit error only to the extent that the net sum of the debit errors is within the debit error value limit that corresponds with your current GST turnover.

So, for example, if your current GST turnover is less than $20 million, the debit error value limit is $12,500; if your current GST turnover is at least $20 million but less than $100 million, the debit error value limit is $25,000.

Tip! Burns Sieber can help you prepare and lodge BASs and assist with correcting errors.

Don’t miss out on fuel tax credits

If you are registered for GST and fuel tax credits, you can claim credits for the excise duty paid on fuel used in eligible business activities. The credits are claimed in your BAS.

This includes fuel used in:

- machinery, plant and equipment;

- light vehicles travelling on private roads or off public roads (you cannot claim for fuel used on public roads);

- heavy vehicles.

Remember to check that you are claiming only for eligible fuels. For example, diesel exhaust fluids (such as Adblue or other additives) are not taxable fuels – they do not attract excise duty so you cannot claim credits for them.

The rate you use depends on:

- when you acquired the fuel (not when you use it);

- the type of fuel;

- the activities it is used for.

You need to apportion your fuel so you are claiming only the fuel tax credits you are entitled to. You need to keep complete records to support your claim and methodology – regardless of the method you use.

Tip! Rates changed on 1 July 2024 and 5 August 2024 so talk to Burns Sieber to ensure you are applying the correct rates.

Are you a small or medium business? Small and medium businesses qualify for a range …